AI summary

Between July 21-23, 2025, Amazon executed a complete global withdrawal from Google Shopping after months of strategic preparation, representing a shift toward owning customer relationships and leveraging its own ecosystem—which now processes over 4 billion monthly product searches. The departure immediately reduced cost-per-click rates by 25-30% across the platform and redistributed significant impression share previously dominated by Amazon (up to 60% in the US). Amazon's exit reflects confidence in its proprietary ad stack and new AI-powered discovery tools (visual search, AR try-ons, multimodal search), while signaling independence from Google and maximizing first-party data retention in a privacy-first era. For advertisers, the result is cheaper clicks but requires strategic repositioning to capture freed inventory and adapt to a reshaped Google Shopping landscape.

Introduction

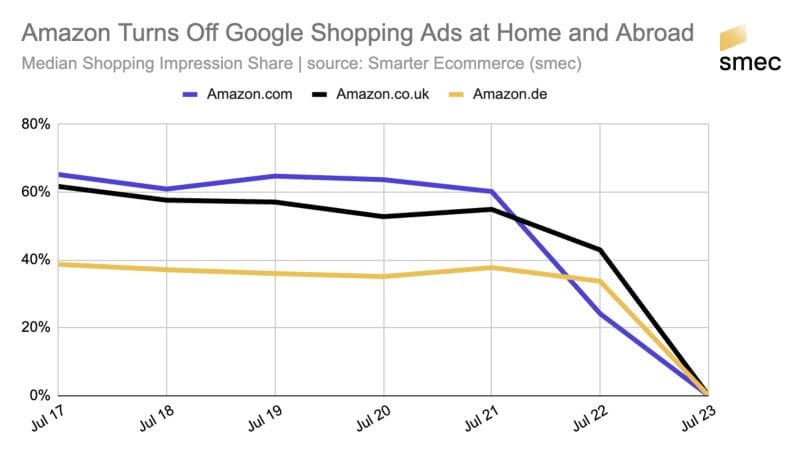

Between July 21 and 23, 2025, Amazon executed a global, total withdrawal from Google Shopping. In less than 48 hours, one of the biggest spenders — controlling up to 60% impression share in the US, 55% in the UK, and 38% in Germany — vanished from Shopping Ads auctions. This move was not a glitch, but the outcome of months of preparation, signaling a decisive strategic shift.

The departure created immediate shockwaves: cost-per-click (CPC) rates collapsed by 25–30%, impressions redistributed, and long-dominant competitors scrambled to capture freed inventory. But beneath the headlines, the implications are far more nuanced. Cheaper clicks do not necessarily mean more profit. Amazon’s exit is as much about its confidence in its own ecosystem as it is about the opportunities — and risks — now facing every other advertiser.

This long-form analysis dives into the how and why behind Amazon’s decision, the measurable impact on Google Shopping, the structural changes and constants, and the practical playbook for brands navigating this new landscape.

Why Amazon exited Google Shopping

A planned, not impulsive, retreat

Amazon’s decision was months in the making. In May 2025, the company cut its US Shopping Ads spend by nearly 50%, using that reduction as a live test. The results confirmed what its executives already believed: that Amazon could sustain acquisition and traffic growth from its own channels, without the dependency on Google. By late July, the global withdrawal was complete. Unlike the temporary pauses during COVID in 2020, this was strategic, comprehensive, and permanent.

Strategic motives behind the move

- Owning customer relationships

By pulling out of Google Shopping, Amazon regained full control of customer acquisition. Historically, Shopping Ads represented a multi-billion-dollar annual expense. Cutting this spend not only boosts margins but also keeps customer data — search intent, browsing, purchase behavior — entirely within Amazon’s walls. In a privacy-first digital era, first-party data is the most valuable currency. - Confidence in its own ecosystem

Amazon has quietly become the world’s second-largest search engine, with over 4 billion product searches per month. The withdrawal is a bold statement: consumers are already starting and finishing their shopping journeys directly on Amazon. With innovations like multimodal search (combining text and image queries), AR shopping features, and the new A10 algorithm rewarding external traffic and engagement, Amazon is no longer just a marketplace — it is a fully-fledged retail search hub. - Efficiency and economics

Google Shopping is expensive, and for Amazon, increasingly marginal. By shifting spend toward its own ad stack (Sponsored Products, DSP, Sponsored Brands), the company gets more precise control of costs and higher lifetime value per shopper. Instead of paying Google for traffic, Amazon can reinvest in better internal personalization and customer retention. - A signal to competitors and regulators

Exiting Google Shopping demonstrates Amazon’s independence and bargaining power. It is no longer tied to Google’s ecosystem for growth. Strategically, this positions Amazon as a peer competitor to Google, not just a marketplace feeding off its traffic.

Why now?

The timing aligns with Amazon’s product roadmap. Over 2024–2025, it rolled out AI-powered discovery tools:

- “Buy for Me”, an AI assistant completing purchases from third-party sites without leaving Amazon’s app.

- Visual search, where users upload an image and instantly see comparable products.

- AR try-ons, designed to replicate the immediacy of in-store shopping.

These innovations gave Amazon the confidence to shut off a major external acquisition channel — proof that it now trusts its ecosystem to self-sustain.

The impact: what changed

CPC relief and visibility gains

Amazon’s sudden absence meant the disappearance of one out of three bids in many retail auctions. CPCs dropped by 25–30% across major categories, and brands reported 15–30% more impressions without increasing spend. New players — mid-market retailers and agile D2C brands — surfaced in Auction Insights for the first time, capturing visibility they could never afford previously.

Rapid share capture by rivals

The vacuum did not last long. Walmart, Target, and Home Depot absorbed about 20% of Amazon’s freed impression share within three days. This illustrates how quickly sophisticated players with deep budgets and feed excellence can seize market share when auctions rebalance.

The “volume trap”

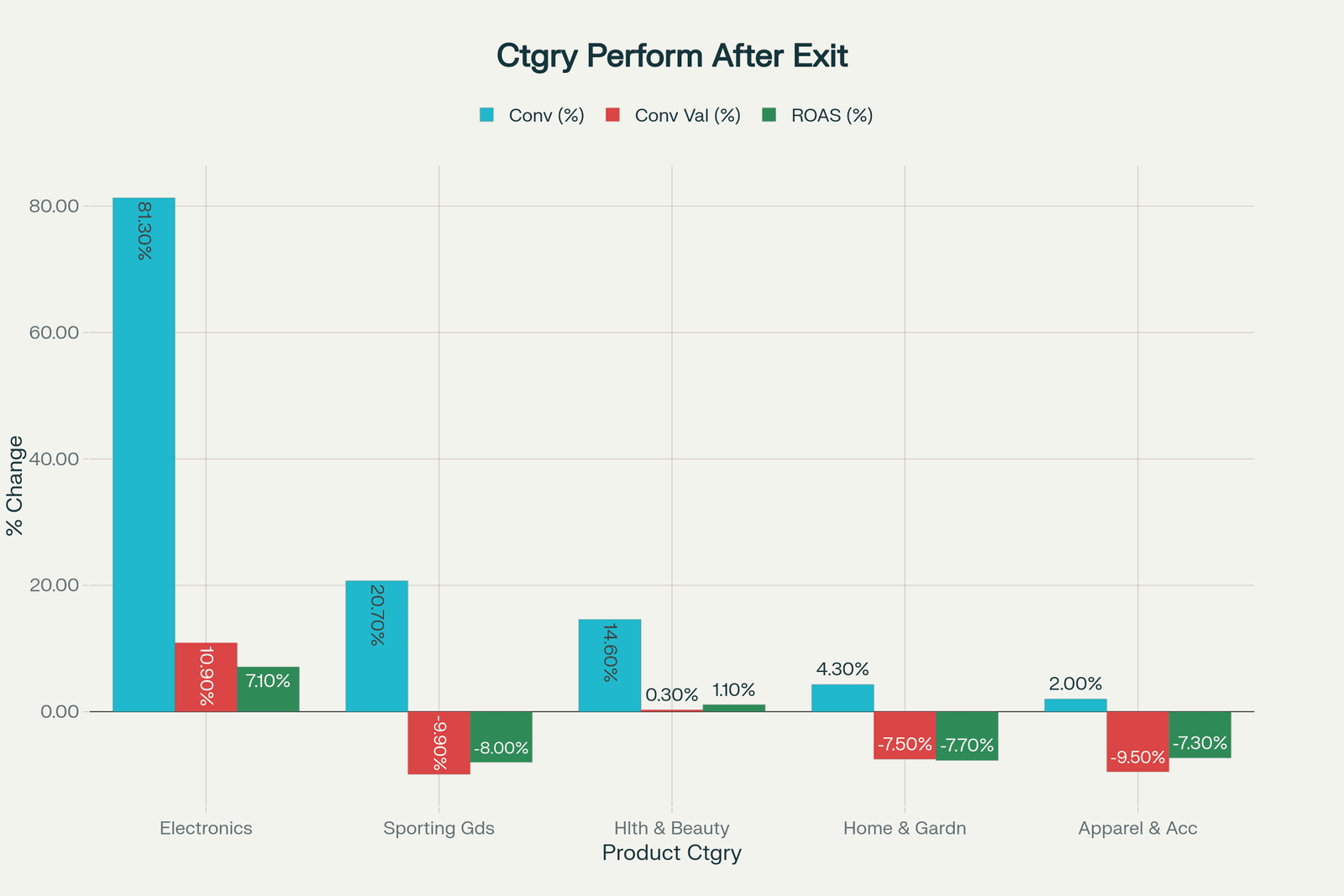

But there is a catch. More clicks at cheaper prices did not automatically translate to more profit. A study of 6,000+ advertiser accounts found clicks rose by nearly 8% on average (up to 18% in some verticals), but conversion value fell 5.5% and ROAS dropped by 4–15%. Why? Because Amazon had been acting as a filter. Its dominance attracted the highest-intent shoppers. When those shoppers clicked on other retailers, many bounced — disappointed by higher prices, longer shipping, or weaker brand trust.

Category differences

- Winners: Electronics retailers like Best Buy matched Amazon’s value proposition, seeing conversion lifts and even small ROAS gains.

- Losers: Apparel, Home & Garden, and Sporting Goods fell into the volume trap. They saw more traffic but struggled to convert it profitably.

Marketplace sellers’ indirect loss

Amazon’s Google Shopping campaigns had also been a source of indirect traffic for sellers on its marketplace. By pulling out, Amazon cut off that external funnel, reducing exposure for thousands of sellers dependent on Google-driven entry points.

What didn’t change

- Google’s Merchant Center rules: GTIN accuracy, taxonomy depth, shipping/tax clarity, and price/in-stock freshness remain critical. Poor feeds are still penalized.

- Smart Bidding fundamentals: Automation principles are unchanged. To sustain results, advertisers still need to supply Google’s machine learning with strong signals: accurate feed data, item-level margins, and conversion values.

- Auction competitiveness: While CPCs fell initially, the laws of supply and demand hold. As rivals step in, prices will normalize. This is a window, not a permanent discount.

What brands can learn

The value of first-party product data

Amazon’s retreat underscores one truth: whoever owns the product data and shopper signals owns the game. Amazon exited Google with confidence because its 1P data ecosystem was robust enough to stand alone. For other retailers, the lesson is urgent: invest in feed enrichment, margin mapping, and real-time availability signals. Data is not just back-end hygiene; it is the lever of competitive advantage.

👉 Where Dataïads platform adds value: This is exactly where solutions like Feed Enrich make the difference. By rich attributes, filling missing product images, and synchronizing pricing and stock in real time thanks to the scraper that incorportae other datasouces to the product feed, brands can transform their raw catalog into a high-performance feed. This ensures ads remain competitive on each platform, surfaces the right products in the right auctions, and provides the foundation for value-based bidding strategies.

Opportunities to seize

- Cheaper scale in the short term

Lower CPCs allow advertisers to cautiously expand: testing more SKUs, entering new geos, or relaxing bid caps without breaking CPA targets. - Feed-led differentiation

Amazon’s absence makes feed quality more decisive than ever. Accurate GTINs, granular variant structuring, and rich attributes (color, material, lifestyle context) can tilt auctions in your favor. - Brand SERP real estate

Without Amazon dominating Shopping slots, brands have a unique window to capture top placements on generic and branded queries alike.

Traps to avoid

- Chasing vanity traffic

More clicks at lower CPCs can destroy ROAS if conversion intent is weak. - Believing CPC relief is permanent

Big-box players are already inflating auctions again. CPC normalization is inevitable. - Competing only on price and delivery

Amazon sets the gold standard. Trying to replicate it is a losing game. Focus on differentiation: curated assortments, local sourcing, sustainability, or superior service.

Recommended playbook

Next 30–90 days

- Audit feed health & feed hygiene: Fill GTIN gaps, enrich attributes, ensure stock/price sync.

- Restructure campaigns: Segment by margin tiers, lifecycle (new/core/clearance), and price bands. Fence broad queries to avoid waste.

- Adopt value-based bidding: Input margin signals into Smart Bidding and test tROAS strategies aligned with profitability.

- Monitor Auction Insights: Weekly track overlap rates, outranking share, and new competitors surfacing.

Next 3–9 months

- Prepare for volatility: Expect CPCs to creep upward as Walmart, Target, and marketplaces pump budgets, especially ahead of Black Friday.

- Diversify acquisition: Use freed budget to test retail media networks (Walmart Connect, Target Roundel), social commerce (TikTok Shop, Meta Advantage+), and organic Shopping SEO.

- Invest in Product Intelligence: Combine product data (attributes, stock, price) with business margins and shopper signals to optimize at product level. This is how you sustain ROAS when CPCs rebound.

Forward-looking projections

- Short-term: CPCs remain lower than pre-exit baselines but rise steadily as competition catches up. Brands with superior feeds and value-based bidding keep ROAS; others regress.

- Seasonal inflection: Expect intensified bidding before Black Friday and Cyber Week. If Amazon re-enters selectively for peak events, auctions could snap back instantly.

- Medium-term: Winners will be those who operationalize item-level economics and scale Product Intelligence. Weak operators will see diminishing returns.

- Strategic: Amazon continues prioritizing its own ad stack and 1P data. Its return to Google Shopping is unlikely to mirror past dominance unless economics shift.

Conclusion

Amazon’s exit from Google Shopping is a once-in-a-decade shake-up. It reduces CPCs, redistributes visibility, and creates new opportunities for agile brands. But it also reveals structural risks: volume without profit, weaker conversion intent, and fast-moving rivals.

For marketers, the message is clear:

- Own and enrich your product data.

- Use value-based bidding tied to real margins.

- Move fast to capture profitable share before CPCs normalize.

- Diversify channels to hedge against volatility and Amazon’s unpredictable moves.

Amazon walked away from Google Shopping because its ecosystem was strong enough to stand alone. For every other advertiser, the task is to build the same resilience — not by imitating Amazon, but by mastering product data and optimizing for sustainable, profitable growth.

👉 Ready to act? Dataïads’ Feed Enrich and Smart Landing Page help brands transform product data into performance — securing long-term ROAS gains in the new post-Amazon era of Google Shopping.